2025 in Review & Outlook for 2026: From Hype to Structure

7 January, 2026

The AI Disruption of SaaS: Which Moats Will Endure

28 April, 2026

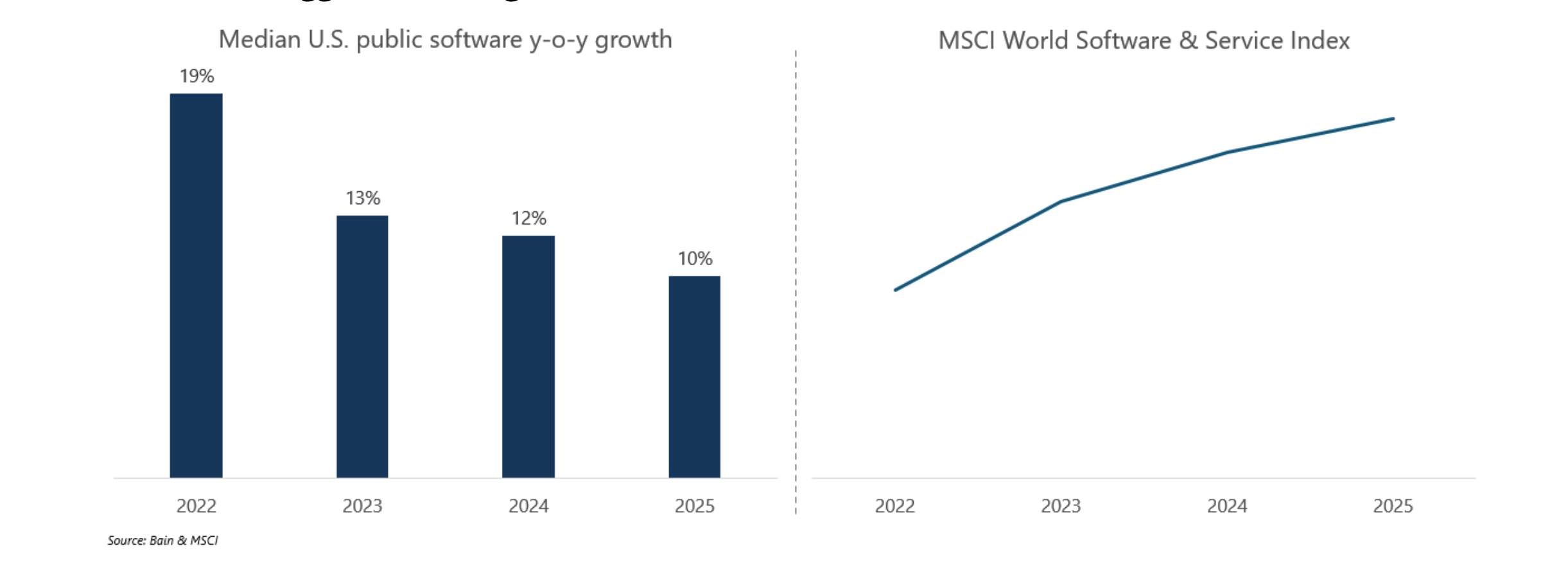

The MSCI World Software & Services Index tumbled by 21% YTD as of 27 Feb 2026. The indiscriminate exodus following the introduction of Claude Cowork reflected growing fears that AI will upend the industry. Here, we attempt to set out a framework for interpreting the market's reactions and the evolving fundamentals of the software sector.

The background

While software growth rates have been declining since 2022, valuations remained elevated till Feb 2026 on the assumption that growth would eventually revert to its historical mean. Valuations supported by the benefit of the doubt, however, are highly sensitive to contradictory evidence. AI presents the most likely scenario to date as to why the good old days may not return. It does not matter that reported financials still look healthy, or that no one knows AI's true impact on the sector given the rapidly changing technology. The threat of a threat is sufficient to trigger a re-rating.

Source: Bain & MSCI

The doomsday scenario

Amid the selloff, some have gone so far as to argue that the demand for software will disappear altogether, as companies vibe-code applications perfectly tailored to their unique needs. In other words, the market is beginning to question the terminal value of software companies.

These fears appear exaggerated. First, developing and maintaining software has little to do with the core business of most companies. Insourcing software spend, which constitutes only <1% of revenue on average (IT budget / company revenue = 3%; SaaS budget / IT budget = 15%), is hardly a justifiable use of resources. A cheaper distraction is still a distraction. Second, a software product is more than just code. Support, customisation, compliance, audit, and integration are all crucial elements to the value proposition.

The structural headwinds at play

Software is not dying, but it is under increasing pressure.

AI has dampened near-term software growth as IT budgets shift from software purchases to token usage and broader transformation projects. Additionally, as AI increases labour productivity and reduces headcount across the economy, the traditional per-seat model, which forms the basis of most SaaS companies' pricing plans, will be impaired.

More importantly, as the cost of writing code continues to fall, replacement cost declines in tandem. The resulting influx of new entrants - unencumbered by legacy systems and emboldened by the paradigm shift - will greatly intensify competition, erode pricing power and margins.

Further, drawn by the lure of owning the cross-functional agent layer, incumbents are likely to expand aggressively into adjacent categories. Boundaries between software categories, and hence budget silos, will likely collapse.

Which economic moats will endure?

In this new competitive reality, the central question is which economic moats will endure.

Economic moats built on inertia, habits, and laziness - qualities AI does not share - are likely to vanish. Interfaces will lose relevance as user habits give way to natural language interactions. Workflows, too, will matter less in a world where underlying models autonomously carry out complex workflows with the help of a markdown file that encodes best practices and domain knowledge. Even the system of record, once considered irreplaceable, is arguably now at risk. With coding agents capable of automating large-scale data migration, switching from Oracle or SAP is no longer unthinkable. Moreover, there is a plausible future in which agents own the execution layer, reducing the canonical system of record to a passive database.

By contrast, software companies that own proprietary data sets procured through exclusive relationships (e.g., Bloomberg), are deeply entrenched in compliance frameworks (e.g., EPIC), or benefit from network effects (e.g., Microsoft 365) are far better positioned to withstand the disruptive forces. This, however, is not a long list.

Essentially, to the exclusion of the few protected by moats anchored in real-world externalities, most incumbents will have to fight vigorously to stay relevant.

Looking forward

While supply expands, demand is likely to rise as well. As improved model capabilities push out the productivity frontier of software, work previously too bespoke or labor-intensive to productise will become addressable by software, pulling spend from adjacent professional services buckets.

Software gross margins will be pressured by higher incremental costs from model inference. That pressure, however, should be offset by a larger pool of absolute gross profits. In that world, software valuations will shift from revenue multiples to gross profit multiples, reflecting both that gross profit is a better proxy for value capture and future free cash flow, and that high gross margins may perversely signal low AI adoption.

There has never been a better time to build software startups. Like cloud computing before it, AI dramatically reduces the cost of building software, while opening new possibilities for product design and go-to-market. Unlike the previous platform shift, AI creates true discontinuities that incumbents' legacy systems cannot accommodate without fundamental rearchitecting. While traditional SaaS is built around human-centric graphic interfaces and deterministic workflows, AI enables conversational interactions with a reasoning engine at the core that orchestrates autonomous agents. The next era of software will be an expression of AI.

SaaS has shifted from a neat stream of annuity to a fluid set of variables. Tools like cohort analysis have become secondary to one central question: how will this SaaS be affected by AI? While public investors may sidestep some of this uncertainty by concentrating on incumbents with the deepest moats, venture investors - who are in the business of backing the audacious intruders - simply do not have that option. Beyond the bare recognition that product features are a necessary but increasingly insufficient condition for success and that greater emphasis should be placed on the ability to execute and build differentiation beyond the codebase, few predictions can be made with confidence given the volatile advance of AI.

In the absence of a crystal ball, the best bet is people. Borrowing liberally from Antifragile by Nassim Nicholas Taleb, those who benefit from disorder are not the ones with the best predictive powers, but the ones who make small bets, learn through trial and error, adapt quickly, and position themselves to seize outsized upside when positive surprises emerge. All hail the transformer (pun intended).

If you are (re)imagining what SaaS could look like, reach out to us at venture@integrapartners.co.

Written by Wang Guanwei, Associate at Integra Partners.